The True State of the Southampton Office Market

07/06/2016

Using Valuation Office Agency data to calculate total stock for Central Southampton (office space of over 1,000 sq ft within Postcode areas SO14,15 and 16), Hellier Langston have produced some analysis to show the true state of supply within the Central Southampton Office Market, and the results are quite startling:

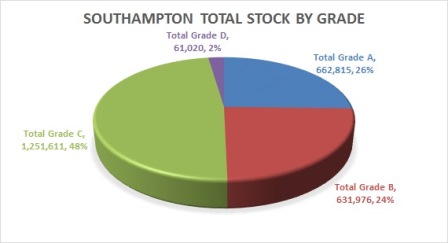

Total Stock for the city stands at just over 2.6m sq ft. Almost 50% of this is Grade C accommodation.

There is a fairly equal split between Grade A, and Grade B, with Grade D space making up only 2% of the total - this is probably because of the loss of poorer quality space to Permitted Development.

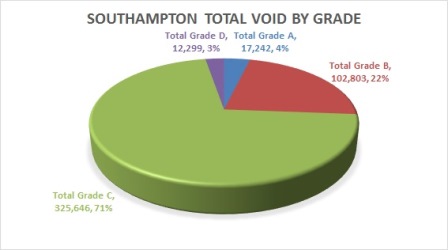

Where the figures start to get interesting, is when this break down of total stock is compared to the relative percentages of Total Void:

As of May 2016, Total void in the City stood at just under 460,000 sq ft, of which Total Grade A was circa 4%, Grade B 22%, and Grade C a massive 71%. Total Void stands at 17.5% of Total Stock.

From these figures, the imbalance between stock and void can be easily made out, with the position of Grade A being the most alarming. Whilst Grade A makes up 25% of Total Stock, it only makes up 3% of Total Void. The rates for Grade B are comparable for both Stock and Void, whilst the vast majority of the Void is Grade C accommodation, which makes up circa 50% of the Total Stock.

In 2015, total 'In town' lettings for offices of over 5,000 sq ft was just under 50,000 sq ft, of which circa 33,000 sq ft (66%) was Grade A accommodation, whilst the remainder was Grade B, with no sizeable lettings of either Grade C or D space.

If demand in 2016 mirrors take-up in 2015, we will be faced with a situation where this imbalance between Stock and Void is exacerbated still further. The winners in this situation will be landlords of existing good quality buildings who can expect strong rental growth. The obvious losers will be tenants who will face higher costs and more limited choice.

The real loser though, might be the City itself. If this imbalance between Stock and Void continues, then the outflow of occupiers such as HSBC from the City Centre will continue, and if existing occupiers cannot be persuaded to stay, what chance is there of attracting new occupiers to relocate to the City?

If demand in 2016 mirrors take-up in 2015, we will be faced with a situation where this imbalance between Stock and Void is exacerbated still further. The winners in this situation will be landlords of existing good quality buildings who can expect strong rental growth. The obvious losers will be tenants who will face higher costs and more limited choice.

Our Offices

Fareham Office

Hellier Langston

Ground Floor

E1 Fareham Heights

Standard Way

Fareham

Hampshire

PO16 8XT

Southampton Office

Hellier Langston

Enterprise House

Ocean Village

Southampton

SO14 3XB